They’re the cornerstones of our economy, but sometimes banks collapse. Why?

Every few years we hear about a bank folding. Why can’t it be prevented? And what’s contagion?

In the wash-up from the global financial crisis, the chief executive of US banking giant JPMorgan Chase, Jamie Dimon, said such shocks were actually not that rare. “Not to be funny about it, but my daughter asked me when she came home from school, ‘What’s the financial crisis,’ and I said, ‘Well, it’s something that happens every five to seven years,’” Dimon told a congressional inquiry in 2010. “We shouldn’t be surprised, but we need to do a better job.”

At the time, the remark from one of the America’s top bankers raised eyebrows, with commentators saying it was flippant. But after the turmoil in global banking of the past few weeks, some finance veterans have a sense of déjà vu.

What started as a crisis in a medium-sized bank in California in early March rocked the wider US banking system and sent shockwaves across the world. Soon after, a crisis in confidence claimed Swiss giant Credit Suisse, with UBS agreeing to buy its rival in a deal arranged hastily by regulators.

The upheaval raises the question of why banks, which play such a fundamental role in the economy, are also prone to occasional bouts of instability? How does contagion spread? And should we just let troubled banks die, as we do with other businesses that don’t work out?

What’s a bank run, and why do they happen?

Economists, always fond of a metaphor, often refer to credit or payment services provided by banks as the lifeblood of the economy. Whether it’s by allowing consumers to store their money safely, or by funding home loans or business investment loans, banks play a fundamental role in keeping the economy functioning.

But throughout history, there have been waves of bank collapses or near-death experiences.

In 1893, a banking panic swept through US cities including Chicago and Los Angeles, which led to 340 banks suspending their operations. Australia also had a banking crisis in 1893, accompanied by a depression; the Reserve Bank has said the crisis caused roughly half the country’s banks to close permanently. In 1907, New York bank the Knickerbocker Trust went bust, sparking The Panic of 1907, which engulfed other banks and helped lead to the establishment of the US Federal Reserve system. And a century later, in 2008, America suffered its biggest banking failure on record when Washington Mutual collapsed after customers rushed to withdraw deposits.

Banking crises can happen for all sorts of reasons because banks deal with lots of risks: the risk of customers not repaying loans, the risk of losses in the value of their financial assets, and the risk of losses from poor systems, scandals or errors.

But one trait that’s peculiar to banks is that their very business model is dependent on the confidence of depositors. Confidence is so crucial because when you deposit money in banks, they don’t simply keep it in a vault; much of the money is used to fund long-term loans, such as 30-year mortgages. As president Franklin D. Roosevelt explained to Americans in 1933, “… the total amount of all the currency in the country is only a small fraction of the total deposits in all of the banks.”

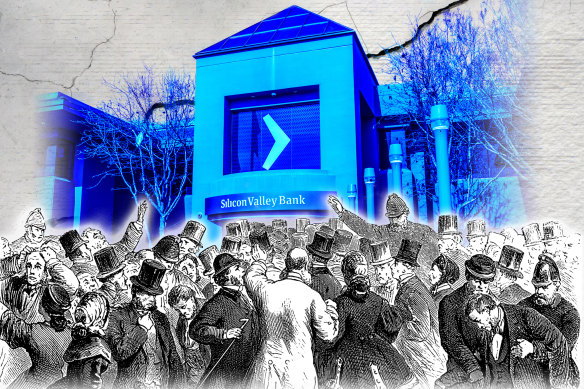

If depositors’ confidence collapses and large numbers of customers withdraw their deposits at the same time, it can trigger a wider panic known as a bank run, as occurred with Silicon Valley Bank recently, causing the second-biggest bank collapse in US history. Banks and regulators go to great lengths to manage the risk of this happening, and Australian authorities have emphasised that our banks are in strong shape.

Technology has made it easier for banking panic to spread, says professor of finance at the University of Melbourne Kevin Davis. These days you can move money out of a bank in a few minutes through an app rather than lining up to withdraw cash, and fears can catch on rapidly through social media.

“Whispers occur via the internet rather than someone telling their neighbour. We’ve moved into a world where it’s easier for contagion to occur,” Davis says.

In financial jargon, contagion refers to a crisis spreading. In the US, the big fear was that SVB’s collapse would prompt people to pull their deposits from other mid-sized banks. Even though SVB was not deemed “systemically important” on its own – not a linchpin of the system – the government was worried enough about these risks to guarantee all its deposits, and to launch a new cheap lending scheme to support other banks’ liquidity.

What do rising interest rates have to do with it?

So, trust matters hugely for banks. But you still need a trigger for a full-blown crisis in confidence to develop. Often, the trigger can be a deterioration in the economy, which can expose problems that may not have been visible when conditions were more buoyant. A well-known quote from investment legend Warren Buffett captures this idea well: “You only find out who is swimming naked when the tide goes out.”

Economies go through cycles – booms and busts. The busts can often involve sectors that were running especially hot in the “boom” phase, such as technology in the case of SVB, or housing in the lead-up to the global financial crisis in the US. A bank might make losses because it is over-exposed to a particular business or industry.

“You think of history, and economic cycles and problems in the economy – they often involve banks in one way or another,” says AMP chief economist Shane Oliver.

The exact causes behind every boom and bust are different. But there are some common factors – and interest rates are a big one.

Often, a period of low interest rates will lead to greater risk-taking by investors and companies and, at the same time, banks might cut their lending standards as they compete for loans. When interest rates rise, more businesses will inevitably struggle because the whole point of raising rates is to slow economic activity. In other words, rate rises necessarily inflict some pain.

In a similar vein to Buffett’s comment about swimming naked, there’s an idea in financial markets that the US Federal Reserve tends to lift interest rates until something breaks. It’s not that they’re setting out to cause problems – their goal is to tame inflation – but parts of the financial system can get into strife as a result.

The chart below from Oliver illustrates the point. It highlights various crises, many of which involved banks, that have occurred after the Fed has jacked up rates in the past five decades or so.

Why can’t we stop these crises from happening?

Major banking crises inevitably lead to new regulations and policies aimed at preventing such instability. For example, the US federal system of bank deposit insurance started in 1934, after a series of damaging bank runs in 1930 that helped cause the Great Depression. The Global Financial Crisis of 2008 also led to a suite of new regulations on banks around the world.

But banking crises still keep on happening. One reason for this, experts say, is that memories fade. Many of the people working at a bank in one crisis might not be there by the time the next one rolls around. With the pain having long receded, Davis says, banks tend to get more involved in risky activities, and hubris can also start to creep in.

At the same time, lobbyists might convince lawmakers to wind back regulation by arguing it’s stifling growth and innovation. SVB, for example, reportedly lobbied the US government to raise a threshold in 2018 that would have forced tougher regulatory scrutiny of the bank.

Another reason is that safeguards to prevent one kind of scenario won’t necessarily apply to the next crisis. For example, the collapse of US investment bank Lehman Brothers in 2008 had lots of causes, but a key one was its involvement in the repackaging of risky home loans. The SVB collapse had very different origins: its heavy exposure to bonds, and reliance on technology start-ups as clients.

Do banks sometimes need to just fold?

Bank failures can have big implications, but experts still argue that troubled banks should be allowed to fail, albeit in a controlled way. That’s because in a capitalist economy, in theory at least, the idea is that successful firms can do well but the weakest won’t always survive. Shareholders profit handsomely if a company is wildly successful, so they should also shoulder the risk of failure.

“When a person buys shares in a company, the risk they take is the company may go under. When a bank goes under, you don’t want to bail out the shareholders because they took the risk,” says Associate Professor Mark Humphery-Jenner from UNSW Business School.

Indeed, if banks knows they always can count on taxpayers coming to the rescue, it might give them the incentive to take on excessive risks in the drive for profits (an issue known as moral hazard).

Compared with other corporate collapses, however, it can be hugely destructive for the economy and individual depositors if large banks are simply allowed to fall over and declare bankruptcy.

Our banking watchdog, the Australian Prudential Regulation Authority (APRA), says it aims to reduce the probability of failure, but it doesn’t run a “zero failure regime”. APRA tries to reduce the chances of a bank failing both by closely supervising individual banks and by looking for wider patterns across the banking system that would raise warning signs.

As well, APRA has the job of ensuring that if a bank were to fail, it would be an “orderly failure”. A speech by a senior APRA official last year said an orderly failure would be one where depositors’ money is safe and the financial system remains stable while shareholders bear the brunt of the pain. Regulators could take over the bank, as they did at SVB, and look to sell off its assets.

In reality, the idea of orderly failure gets a lot harder with larger institutions, which have linkages all over the world’s financial system and greater potential to cause instability.

Lehman Brothers was allowed to fail in 2008, and that day is seen as the climax of the global financial crisis. Whether this was the right call has been heavily debated, but the bankruptcy unleashed chaos on global markets and is likely to have deepened the recession in the US.

When Credit Suisse was teetering in mid-March, Swiss regulators were not prepared to let the bank fail. Instead, they brokered a deal with its rival UBS once they reached the conclusion that Credit Suisse could not recover from its troubles.

Regulators, who heavily supported the deal, said they had to act to avoid inflicting serious damage on Swiss and international financial markets. “It was indispensable that we acted quickly and find a solution as quickly as possible,” said Swiss National Bank president Thomas Jordan.

Fascinating answers to perplexing questions delivered to your inbox every week. Sign up to get our Explainer newsletter here.

Most Viewed in Business

Source: Thanks smh.com